Note: An updated version of this paper was published March 14, 2024.

Incarceration, or confining people in jail or prison, is a significant state revenue expense in Tennessee’s budget. This report provides context for discussions about criminal justice reform by examining the budgetary aspects of incarceration in Tennessee.

A companion report looks at historical trends in Tennessee’s incarcerated and corrections populations. Two additional reports will focus on community supervision, prison releases, and recidivism as well as pre-trial incarceration.

Key Takeaways

- Funded almost entirely by state revenues, the Tennessee Department of Correction (TDOC) is consistently among the state’s six largest state revenue expenses.

- Incarceration costs make up over 80% of TDOC spending.[i]

- Since FY 1995, TDOC spending increased by an average of 4.1% per year — the same as growth in overall state revenue spending.[i]

- TDOC houses 27% of state prisoners in local jails to manage overcrowding in state facilities, a factor in slowing the growth of the department’s budget.

The Tennessee Department of Correction’s Budget

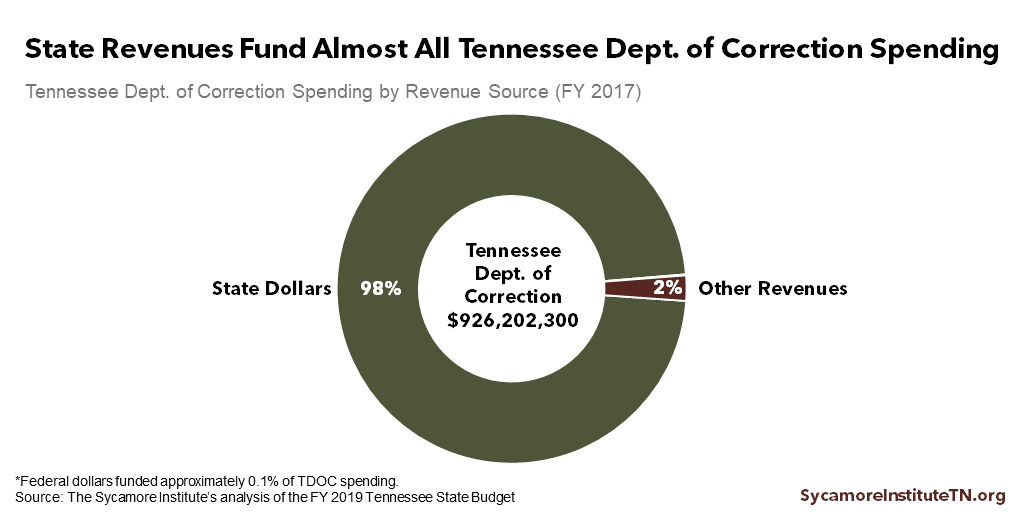

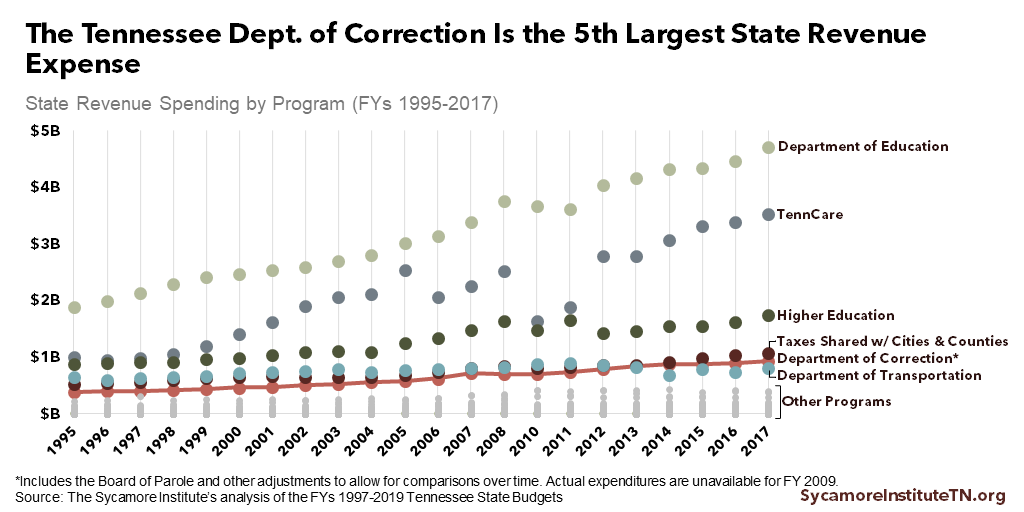

Funded almost entirely by state revenues, the Tennessee Department of Correction (TDOC) is consistently among the state’s six largest state revenue expenses. (1) In FY 2017, state revenues accounted for 98% of TDOC’s $926 million budget (Figure 1). The department was the 5th largest state revenue expense that year behind K-12 education, TennCare, higher education, and taxes shared with cities and counties (Figure 2). Nationwide, 12 states spend a larger share of state revenue on corrections than Tennessee. (2)

TDOC spending and overall state revenue spending have grown at the same pace in recent decades. (1) TDOC’s budget1 and overall state revenue spending both grew by an average of 4.1% per year from FY 1995-2017. Adjusted for inflation, both measures have increased 63% since FY 1995 — an average of 2.2% annually.

State prisoners, felony incarcerations, and state incarcerations — In this report, these terms refer to inmates under the jurisdiction of the Tennessee Department of Correction (TDOC). These are convicted state felony offenders sentenced to reside in either state prisons or local jails.

Figure 1

Figure 2

Incarceration Costs in TDOC’s Budget

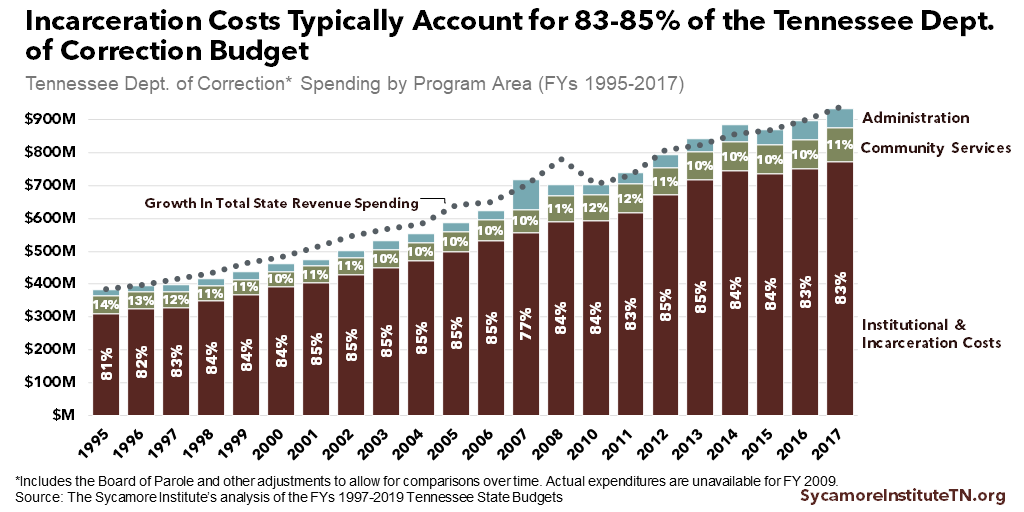

Incarceration costs typically account for 83-85% of TDOC spending (Figure 3).[ii] (1) Factors — some outside the regular budget process — that drive these costs include crime rates, policing practices, prosecutions, sentencing, time served, the health care needs of incarcerated populations, and recidivism.

Policymakers have slowed the growth of incarceration spending with nearly $200 million in TDOC base budget reductions over the last 11 years. (3) These reductions were primarily a result of policy changes aimed at slowing inmate population growth, such as sentencing changes and greater use of community supervision. (4) In some years, diverting inmates from local jails to empty state prison beds also yielded savings. (5)

Figure 3

Budget Effects of Incarcerating State Prisoners in Local Jails

TDOC houses 27% of state prisoners in local jails to manage overcrowding in state facilities, a factor in slowing the growth of the department’s budget. To house every state prisoner in a state facility would require an extra $648 million to build new prison capacity and an extra $88 million per year in operating costs, according to a 2017 study by the Tennessee Advisory Commission on Intergovernmental Relations (TACIR). (6)

TDOC pays local governments a per diem for housing state prisoners. The per diem amounts are capped in each year’s state funding bill, and almost every county gets a max of $39.00 per prisoner per day in FY 2019. (6) Counties can also contract with the state and negotiate separate rates. As of FY 2017, three of the six counties that did so received less than the daily max and three got more, ranging from $25.25 in Rhea County to $69.60 in Shelby County. (6) Local governments are only reimbursed for convicted and sentenced felony offenders — not inmates awaiting trial, sentencing, or probation violation hearings. (6)

Lower Costs for TDOC, Fewer Services for Inmates

In most cases, these per diem payments cost TDOC less than housing inmates in state prisons. In FY 2019, for example, the estimated average daily cost to house a prisoner in a TDOC facility is $76.83 (ranging from $54.77 to $170.64 per day depending on the facility). (7) That is almost twice the standard max per diem of $39.00.

In at least some counties, per diems may not fully cover the cost of housing state prisoners. Reliable data are unavailable, but TDOC estimated in 2016 that local jails’ costs were likely around $44.00 per prisoner per day. (6) That is less than TDOC facility costs but more than the per diems paid by the state.

Most local jails do not provide the same level of services and programs that are available at state prisons. The 2017 TACIR study found local jails typically offer fewer mental health, substance abuse, education, and reentry programs, and some do not meet minimum quality standards. (6) TACIR also noted TDOC studies that show “recidivism is higher among state prisoners released from jails rather than prisons.”

Figure 4

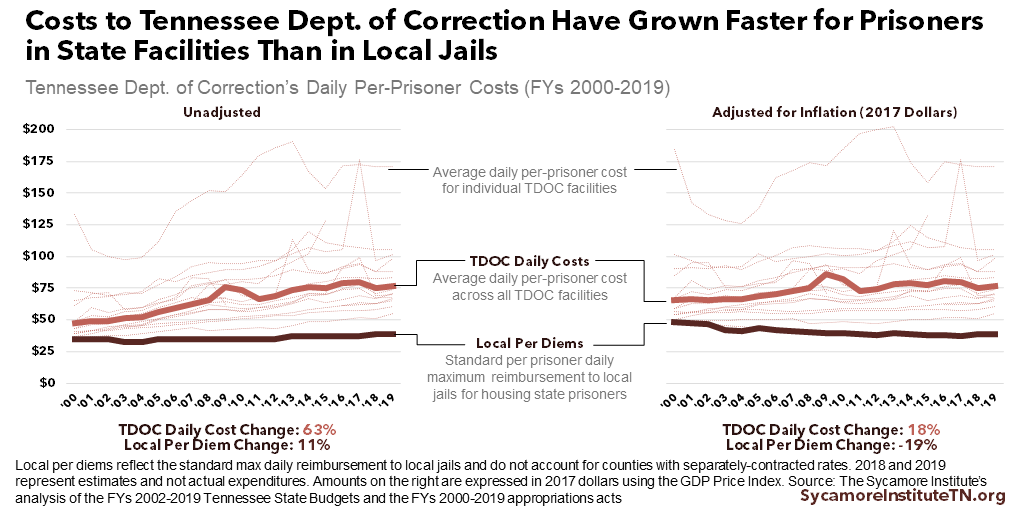

Comparing TDOC Costs Over Time

The cost of housing inmates in state facilities has risen faster than TDOC’s per diem payments to local governments (Figure 4). Local jail per diems grew 11% between FY 2000-2019, compared to a 63% increase in TDOC facilities’ daily per-prisoner costs. (1) (8) Over that period, the standard per diem rose from $35.00 per prisoner per day to $39.00 while average TDOC facility costs went from $47.16 to an estimated $76.83. Adjusted for inflation, standard local per diems fell 19% while average TDOC facility costs increased by 18%.

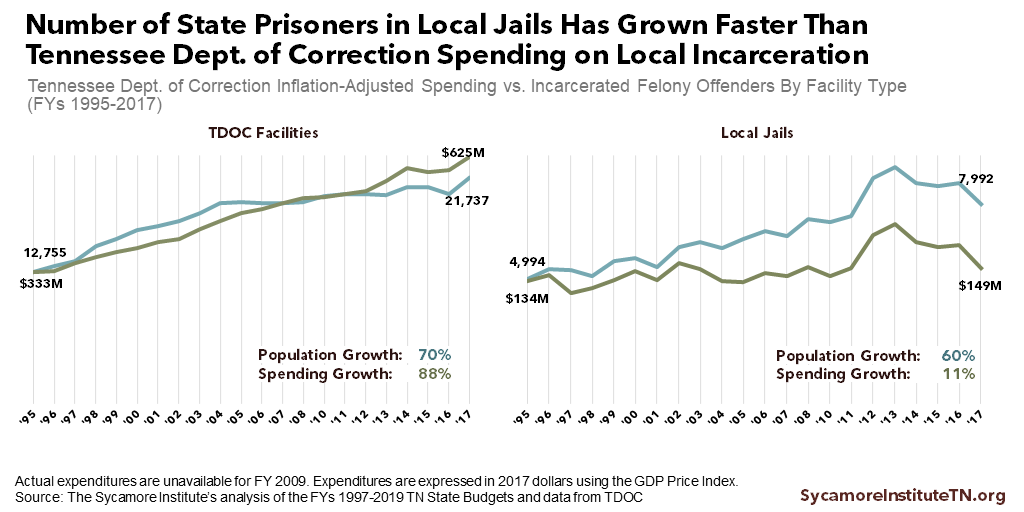

The number of state prisoners in local jails has grown faster than TDOC spending on local incarcerations (Figure 5). Local incarcerations of state prisoners increased 60% from FY 1995-2017 while TDOC’s inflation-adjusted costs grew by 11%. In contrast, the state prisoner population in TDOC facilities rose 70%, while inflation-adjusted spending for these facilities grew by 88%. (1) (9) As a result, local incarceration costs are a declining share of TDOC’s total incarceration spending (Figure 6). (7)

Figure 5

Figure 6

Background: 1985 Tennessee Corrections Reforms

In the 1980s, Tennessee made significant reforms and investments to address state prison facility conditions. Throughout the 1970s and 1980s, overcrowding, poor sanitation, and poor medical care in state facilities led to multiple prison riots and federal lawsuits. The federal government even oversaw the state prison system for a time, and a federal judge halted all new entries into state prisons until overcrowding was addressed. (13)

The Tennessee General Assembly held a special session on corrections in November 1985 to address these issues. New laws passed in this session allow the governor to declare an overcrowding emergency, created a commission to revise sentencing laws, established new alternatives to incarceration, and increased funding by over $320 million to improve and expand state prison capacity. (6) (13) (14)

Lawmakers also created new funding requirements meant to help prevent overcrowding in the future. Under the state constitution, any new law without its first-year cost funded in the budget becomes void. (12) The Sentencing Act of 1985 set an even higher standard for new laws expected to increase periods of imprisonment in state facilities. In such cases, the budget must pre-fund the highest-cost year expected over the next decade. (11)

Footnotes

[i] Historical analyses of TDOC funding include adjustments to allow for comparisons over time. These reflect reorganizations of funding for parole/probation and TRICOR. The historical data displayed in this report include TDOC’s budget plus the Board of Parole/Probation’s budget less any funding for TRICOR/Correctional Enterprises that was in TDOC’s budget in FYs 1995 and 1996.

[ii] TDOC expenditures were categorized in the following ways:

- Incarceration costs include all institutional costs for TDOC-run, specialty, and contract facilities as well as local incarceration costs under the State Prosecutions and Local Jail Boarding Fees line items.

- Community services costs include all line items associated with community-based programs and probation and parole boards and supervision — including the Sex Offender Treatment, Correction Release Centers, Community Corrections, Community Service Centers, Local Correctional Programs, and Community Supervision line items.

- Administrative/other includes all other costs — including Administrative Services, Tennessee Correction Academy, and Major Maintenance.

References

Click to Open/Close

- State of Tennessee. Tennessee State Budgets for FY 1997 through FY 2019. [Online] Accessed from https://www.tn.gov/finance/fa/fa-budget-information/fa-budget-archive.html.

- The Sycamore Institute’s analysis of data from the National Association of State Budget Officers. State Expenditure Data for 1991-2018. [Online] 2018. Historical data downloaded from https://www.nasbo.org/mainsite/reports-data/state-expenditure-report on January 3, 2019.

- State of Tennessee. FY 2014 Tennessee State Budget, Vol. 2, p.59 (“6-Year Recurring Base Reduction Summary”) and FY 2019 Tennessee State Budget, Vol. 2, p.9 (“8-Year Recurring Base Reduction Summary”). [Online] Accessed from https://www.tn.gov/finance/fa/fa-budget-information/fa-budget-archive.html.

- State of Tennesssee. Vol. 2 Base Budget Reductions for FY 2010 through FY 2019 . [Online] Accessed from https://www.tn.gov/finance/fa/fa-budget-information/fa-budget-archive.html.

- State of Tennessee. Vol. 2 Base Budget Reductions for FY 2010 . [Online] 2010. https://www.tn.gov/finance/fa/fa-budget-information/fa-budget-archive/fa-budget-publication-2009-2010.html.

- Tennessee Advisory Commission on Intergovernmental Relations (TACIR). Housing Tennessee’s Convicted Felons: Improving Outcomes while Balanacing State and County Needs. [Online] 2017. https://www.tn.gov/content/dam/tn/tacir/documents/2017HousingTNConvictedFelons.pdf.

- State of Tennessee. FY 2019 Tennessee State Budget. [Online] 2018. https://www.tn.gov/finance/fa/fa-budget-information/fa-budget-archive/fa-budget-publication-2018-2019.html.

- —. Annual Appropriations Acts for FY 2002 through FY 2019. [Online] Accessed from https://sos.tn.gov/division-publications/acts-and-resolutions.

- Tennessee Department of Correction (TDOC). Tennessee Felon Population Updates for 2006-2018. [Online] 2006-2018. Accessed from https://www.tn.gov/correction/statistics-and-information/felon-population-reports.html

- —. Tennessee Jail Summary Reports for 2000-2018. [Online] 2000-2018. Accessed from https://www.tn.gov/correction/statistics-and-information/jail-summary-reports.html.

- State of Tennessee. TN Code § 9-4-210 (2017). [Online] 2017. https://law.justia.com/codes/tennessee/2017/title-9/chapter-4/part-2/section-9-4-210/.

- —. State Consistution Article II Section 24. [Online] http://www.capitol.tn.gov/about/docs/TN-Constitution.pdf.

- Tennessee State Library and Archives. Agency History: Tennessee Prison System (1831-1992). [Online] https://sos-tn-gov-files.tnsosfiles.com/forms/TENNESSEE_STATE_PRISON_RECORDS_1831-1992.pdf.

- Tennessee Department of Correction (TDOC). Historical Timeline: 1700-2013. [Online] https://www.tn.gov/content/dam/tn/correction/documents/HistoricalTimeline.pdf.