Key Takeaways

- Major differences in the enacted budget vs. the governor’s recommendation include more money for franchise tax refunds, a potential FY 2024 revenue deficit, and new spending funded mainly by higher expected treasury investment earnings.

- Compared to the governor’s initial proposal, these changes increase spending from state revenues by $92 million or 0.3% in FY 2024 and by $301 million or 1.2% in FY 2025.

- The final budget includes $144 million for Education Freedom Scholarships. As lawmakers did not pass a bill to create that program, those funds can’t be spent but will remain in the base budget.

- The enacted budget includes a $100 million deposit to the state’s rainy day fund in FY 2025 — $80 million more than the governor proposed in February.

In late April, the General Assembly amended and approved Tennessee’s FY 2025 budget, which starts July 1, 2024. The enacted budget included revisions from the governor and legislature to the original February budget plan for FYs 2024 and 2025. The changes reflect new revenue information, program needs, and legislative action. Compared to the recommendation, these changes boost spending and allocations from state revenues by $92 million or 0.3% in FY 2025 and by $301 million or 1.2% in FY 2025.

This summary highlights key changes and developments since February. (1) (2) (3) (4) (5)

Overview

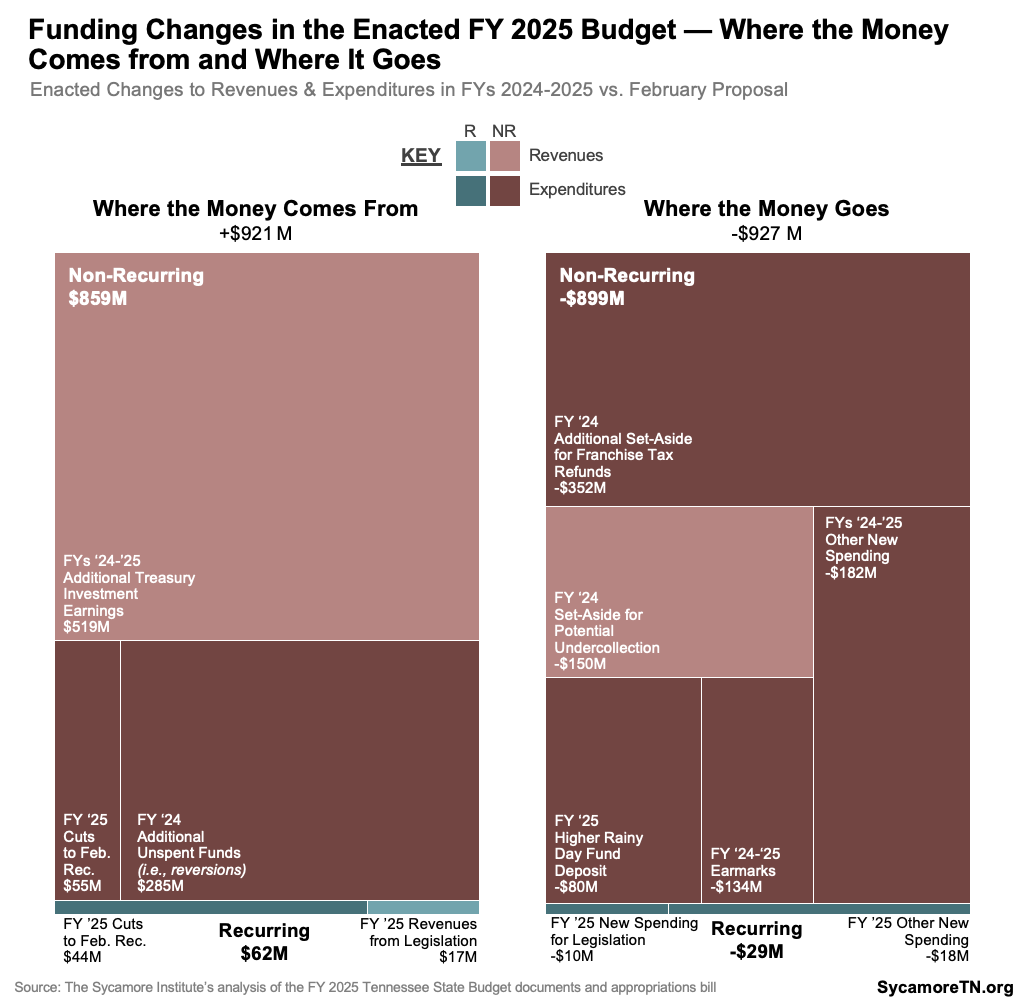

Compared to the February proposal, the enacted budget includes more money for franchise tax refunds, a potential FY 2024 revenue deficit, and new spending—funded mainly by higher expected treasury investment earnings (Figure 1). Together, this boosts spending from state revenues to an estimated $32.1 billion in FY 2024 and $25.7 billion in FY 2025.

Figure 1

Where the Money Comes From

Compared to the governor’s initial recommendation, the enacted budget includes:

- $519 million more in non-recurring revenue from additional expected earnings on the treasurer’s investment of state funds—including $505 million in FY 2024 and $14 million in FY 2025. These earnings have been unusually high in recent years due to the billions the state received in federal COVID-related relief. Many of those dollars don’t expire for years, allowing the state to invest them until they are spent.

- $285 million more (non-recurring) in FY 2024 from agencies reverting unspent money to the General Fund.

- $99 million in reductions to programs and initiatives proposed in February, including $44 million in recurring and $55 million in non-recurring funds. The largest changes are the elimination of $31 million in recurring funds previously proposed to replace federal dollars for summer learning programs and $25 million in non-recurring funds for a proposed farmland conservation fund.

- $17 million in recurring revenues from the impact and re-estimates of new laws affecting revenues.

Where the Money Goes

Compared to the governor’s initial recommendation, the enacted budget includes:

- $352 million in additional non-recurring funding in FY 2024 to issue refunds associated with the franchise tax cut discussed below.

- $150 million non-recurring in case FY 2024 tax collections underperform the revised projection in February’s budget (discussed below).

- $136 million in earmarked grants for specific organizations and projects—including $1 million recurring and $134 million non-recurring (discussed below).

- $80 million to increase the FY 2025 non-recurring deposit to the rainy day fund to $100 million(discussed below).

- $209 million in additional spending for new legislation and other programs—including $28 million recurring and $182 million non-recurring (discussed below).

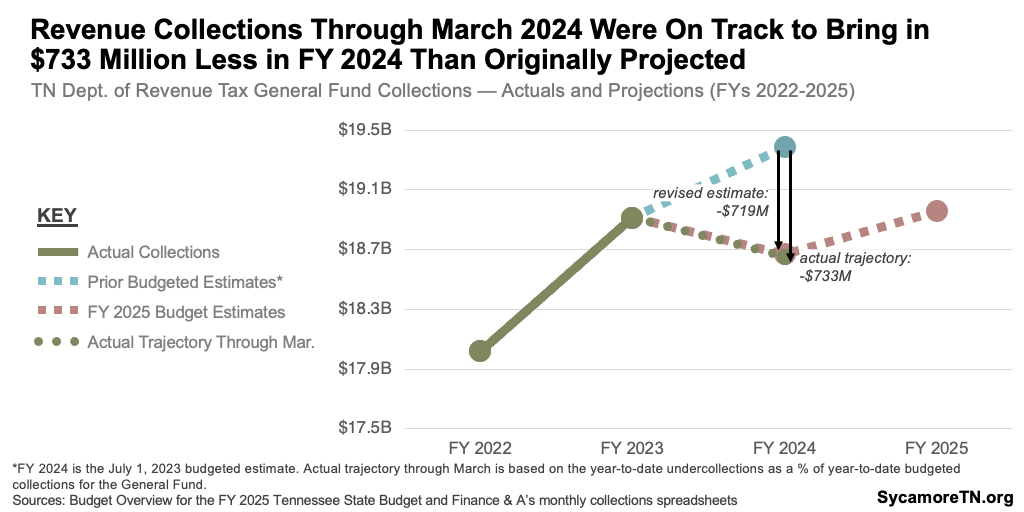

Tax Collections

The enacted budget braces the state for even lower FY 2024 tax collections than the revised estimate in the February recommendation. The February budget anticipated collecting about $719 million less in revenue than initially planned for FY 2024. The trajectory of actual collections through March was $733 million less than originally projected for the year and $14 million less than February’s revised estimate (Figure 2). (6) The enacted budget sets aside another $150 million in non-recurring revenues to close the year if revenues underperform the revised projection.

Figure 2

Franchise Tax Cut

Policymakers approved a revised version of the governor’s franchise tax cut. Under prior law, businesses paid either 0.25% of net worth or 0.25% real and tangible property in Tennessee—whichever was higher. The tax on property was considered an alternative minimum. Key features of the final agreement include: (7) (8) (9) (10)

-

- Permanent Tax Cut – As the governor proposed, the new law eliminates the alternative minimum tax on property—leaving only the tax on net worth.

- Refunds – Businesses that paid the alternative minimum on property are eligible for a refund for the difference between what they paid and what would have been paid on net worth and only for tax periods ending on or after March 31, 2020. Companies must file refund claims between May 15 and November 30, 2024. Refunds will not cover attorney fees.

- Public Reporting – Between May 31 and June 30, 2025, the Department of Revenue will post online all businesses receiving a refund, categorized based on refund size: $750 or less, $751-10,000, more than $10,000, and a category with no amount for any pending refunds. Available information suggests that some refunds could be hundreds of thousands of dollars.(11)

- Legal Restrictions – Businesses claiming a refund must waive the right to sue for additional damages related to the alternative minimum tax.

The enacted budget sets aside $1.6 billion in FY 2024 for refunds and assumes a $393 million reduction in recurring tax collections in FY 2025. The enacted budget reconciled the administration’s estimates of the original proposal with the legislature’s. The $1.6 billion refund account is $352 million more than the February proposal. The $393 million impact in FY 2025 is $17 million less than before. Beginning in FY 2026, the recurring annual revenue reduction is expected to be $405 million. Any unspent refund dollars will revert to the General Fund on July 1, 2026, for reallocation in future years. (8) (3) (9)

Earmarked Grants

The enacted budget includes $136 million ($1.4 million recurring and $134.4 million non-recurring) for 68 targeted grants to specific communities and organizations in FYs 2024 and 2025. The largest is $50 million to relocate the Tennessee Performing Arts Center (TPAC) to Nashville’s East Bank—on top of the $200 million approved in the FY 2024 budget. Other significant earmarks include $17 million to replace an unspent expiring grant for the Nashville raceway and $12 million for the relocation of the Brooks Museum of Art in Memphis.

Education Freedom Scholarships

Lawmakers did not agree on Gov. Lee’s proposed Education Freedom Scholarship Act. The General Assembly did not enact any of the proposed versions of the bill. All three versions had small differences in key details like low-income thresholds and scholarship calculation, but more significant differences across the three included:

- Lee’s version proposed 20,000 scholarships of up to $7,075 per student for private school attendance and expenses in FY 2025. In this version, the program would become universal in FY 2026, depending on the funding availability.(12) (13)

- The Senate considered versions allowing students to use the scholarships to attend public schools in other districts.(14) (15) (16) (17)

- The House version included the private school scholarships, plus additional state funding for small and sparse school districts and teacher health insurance premiums. It also would have scaled back state assessment and teacher evaluation requirements.(18) (19)

Since lawmakers did not pass a bill to create the program, the enacted budget’s $144 million recurring for Education Freedom Scholarships will go unspent but remain in the base budget. The General Assembly passed the FY 2025 budget with the $144 million in funding proposed by the governor in February before negotiations on the proposal fell apart. Those funds cannot be spent on the scholarships without a general law change setting up the program. However, this means $144 million is already accounted for in the starting base for this purpose for the FY 2026 budget process.

Figure 3

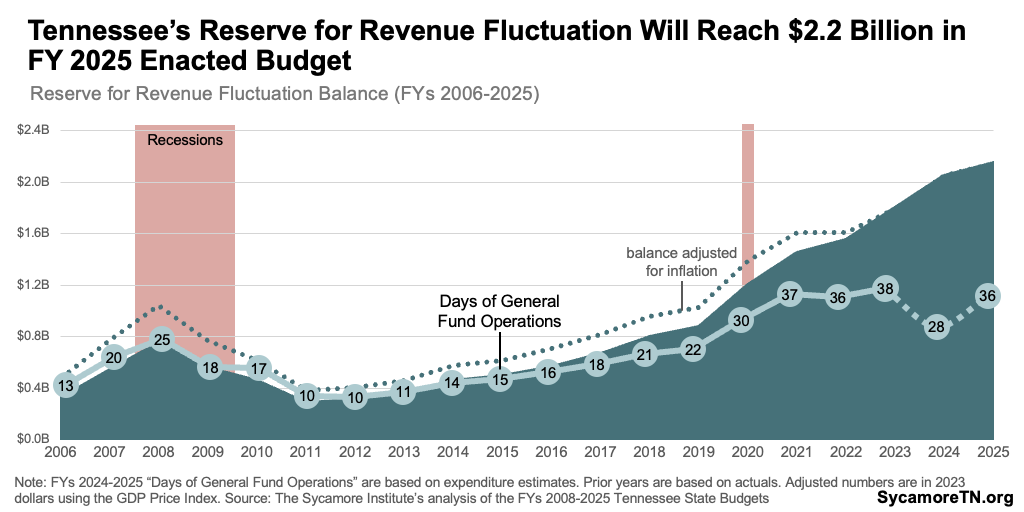

Rainy Day Fund

The enacted budget includes a $100 million deposit to the state’s rainy day fund in FY 2025—$80 million more than proposed in February.[1] This deposit will bring the Reserve for Revenue Fluctuation balance up to $2.2 billion by the end of FY 2025, the highest ever (Figure 3). This balance would cover about 38 days of state-funded General Fund operations at the enacted FY 2025 levels. This is about 11 days more cushion than just before the Great Recession.

Other New Spending

The final budget included $209 million in additional spending for new legislation and other programs not in the February recommendation. Several of the largest new spending items include:

- $86 million non-recurring for additional capital projects—including $40 million for improvements at the I-24 industrial site in Coffee County and $30 million for an anatomy lab at the UT Health Science Center.

- $15 million in non-recurring grants for purchasing fire, rescue, and emergency management services equipment.

- $15 million non-recurring for two economic development funds—including $10 million for a nuclear development fund and $5 million for a film incentive fund.

- $8 million recurring to fund several new laws expected to increase incarceration costs.

- $6 million non-recurring to offset the costs of deploying the Tennessee National Guard to the U.S. Southern border in Texas—including $1 million for FY 2024 and $5 million for FY 2025. The General Assembly authorized the governor to deploy 2,000 or more soldiers under separate legislation.(22) (23)

[1] Our analyses of the state’s rainy day fund typically also includes the TennCare Reserve, which has also been used in the past to respond to economic downturns. However, FY 2025 budget documents show that a significant portion of those balances are already obligated for specific purposes (e.g., shared savings, IT improvements), so we have excluded them from this summary.

References

Click to Open/Close

- Tennessee Department of Finance and Administration. State of Tennessee, The Budget Fiscal Year 2024 – 2025. Fiscal Year 2024-2025 Budget Publications. [Online] February 5, 2024. [Cited: February 5, 2024.] https://www.tn.gov/finance/fa/fa-budget-information/fa-budget-archive/fiscal-year-2024-2025-budget-publications.html.

- —. Budget Overview to the FY 2024-2025 State Budget. [Online] February 5, 2024. https://www.tn.gov/content/dam/tn/finance/budget/documents/overviewspresentations/FY25%20Budget%20Overview%20Final.pdf.

- —. Fiscal Year 2024-2025 Administration Budget Amendment Overview . Current Budget Overviews & Presentations. [Online] March 3, 2024. [Cited: April 29, 2024.] https://www.tn.gov/finance/fa/fa-budget-information/fa-budget-overviews_presentations.html.

- Hazlewood, Rep. Patsy. House Finance, Ways, and Means Amendment 3 to HB 2973. Tennessee General Assembly. [Online] April 2024. https://www.capitol.tn.gov/Bills/113/Amend/HA1042.pdf.

- Tennessee General Assembly. Finance, Ways, and Means Action on FY 2024-2025 Appropriations Bill HB 2973/SB 2942. House Dashboard. [Online] April 16, 2024. https://www.capitol.tn.gov/Archives/Dashboard/HR%20Scanned%20Amendments/HB2973_House%20Schedule%204.16.24.1430.pdf.

- Tennessee Department of Finance and Administration. February Revenues. [Online] March 18, 2024. https://www.tn.gov/finance/news/2024/3/18/february-revenues.html.

- Tennessee General Assembly. Conference Committee Report on House Bill No. 1893 / Senate Bill No. 2103. [Online] 2024. [Cited: 29 2024, April.] https://www.capitol.tn.gov/Bills/113/CCRReports/CC0008.pdf.

- —. HB 1893 – SB 2103 Bill Summary. [Online] [Cited: April 29, 2024.] https://wapp.capitol.tn.gov/apps/BillInfo/Default.aspx?BillNumber=HB1893&GA=113.

- Fiscal Review Committee Staff. Fiscal Note HB 1893 – SB 2103. Tennessee General Assembly. [Online] February 12, 2024. [Cited: April 29, 2024.] https://www.capitol.tn.gov/Bills/113/Fiscal/HB1893.pdf.

- Jones, Vivian. Tennessee House, Senate reach deal on franchise tax bill — including public disclosures. The Tennessean. [Online] April 25, 2024. [Cited: April 29, 2024.] https://www.tennessean.com/story/news/politics/2024/04/25/tennessee-house-senate-reach-compromise-on-franchise-tax-deal/73437952007/#.

- —. Majority of $1.5B Franchise Tax Refunds Would Flow Out of Tennessee, New Records Show. The Tennessean. [Online] April 23, 2024. https://www.tennessean.com/story/news/politics/2024/04/23/majority-of-1-5-billion-franchise-refunds-set-to-go-out-of-tennessee-records-show/73414899007/.

- Lundberg, Sen. Jon. Senate Education Amendment 1 to SB 0503 (014256). Tennessee General Assembly. [Online] March 2024. https://www.capitol.tn.gov/Bills/113/Amend/SA0583.pdf.

- Fiscal Review Committee Staff. Fiscal Memorandum: SB 503 – HB 1183 (014256, 018520). Tennessee General Assembly. [Online] April 16, 2024. https://www.capitol.tn.gov/Bills/113/Fiscal/FM2955.pdf.

- Lundberg, Sen. Jon. Senate Education Amendment No. 2 to SB 0503. Tennessee General Assembly. [Online] 2024 March. www.capitol.tn.gov/Bills/113/Amend/SA0584.pdf.

- Fiscal Review Committee Staff. Fiscal Memorandum: SB 503 – HB 1183 (014400). Tennessee General Assembly. [Online] February 26, 2024. https://www.capitol.tn.gov/Bills/113/Fiscal/FM1770.pdf.

- Lundberg, Sen. Jon. Senate Education Amendment No. 3 to SB 0503. Tennessee General Assembly. [Online] March 2024. https://www.capitol.tn.gov/Bills/113/Amend/SA0630.pdf.

- Fiscal Review Committee Staff. Fiscal Memorandum: SB 503 – HB 1183 (015064, 018520). Tennessee General Assembly. [Online] April 16, 2024. https://www.capitol.tn.gov/Bills/113/Fiscal/FM2956.pdf.

- White, Rep. Mark. House Education Administration Amendment No. 1 to HB 1183. Tennessee General Assembly. [Online] March 2024. https://www.capitol.tn.gov/Bills/113/Amend/HA0653.pdf.

- Fiscal Review Committee Staff. Fiscal Memorandum: SB 503 – HB 1183 (015320, 017387). Tennessee General Assembly. [Online] March 28, 2024. https://www.capitol.tn.gov/Bills/113/Fiscal/FM2714.pdf.

- U.S. Bureau of Labor Statistics. Comparing the Consumer Price Index with the Gross Domestic Product Price Index and Gross Domestic Product Implicit Price Deflator. Monthly Labor Review. [Online] March 2016. https://www.bls.gov/opub/mlr/2016/article/comparing-the-cpi-with-the-gdp-price-index-and-gdp-implicit-price-deflator.htm.

- U.S. Bureau of Economic Analysis. Gross Domestic Product: Chain-type Price Index [GDPCTPI], retrieved from FRED, Federal Reserve Bank of St. Louis. [Online] January 2024. https://fred.stlouisfed.org/series/GDPCTPI.

- Tennessee General Assembly. HB 2190 – SB 2538. [Online] April 2024. https://wapp.capitol.tn.gov/apps/BillInfo/Default.aspx?BillNumber=HB2190.

- Fiscal Review Committee Staff. Fiscal Memorandum: HB 2190 – SB 2538. Tennessee General Assembly. [Online] March 20, 2024. https://www.capitol.tn.gov/Bills/113/Fiscal/FM2593.pdf.