Medical debt is surprisingly common and can have far-reaching effects on prosperity and health. This report looks at the estimated prevalence of medical debt in Tennessee and explains why it matters. A companion report provides background on how medical debt occurs. Future reports will focus on how medical debt varies across Tennessee’s 95 counties and options for policymakers who want to address it.

Key Takeaways

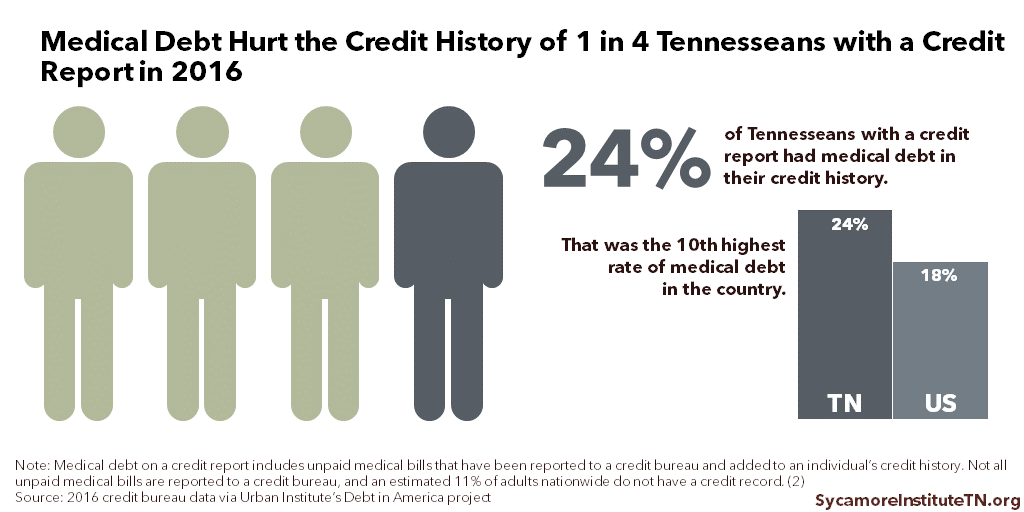

- 24% of Tennesseans with a credit report had medical debt on their credit history in 2016 – the 10th highest rate in the country. The median amount of medical debt on their credit reports was $739.

- Available data suggest medical debt is common across most demographic and socioeconomic groups in Tennessee but more so among the uninsured, those with lower incomes or education levels, and people of color.

- Even small amounts of medical debt can hinder economic security and mobility by feeding debt cycles and reducing access to jobs, housing, and forms of credit that help build wealth.

- People with medical debt are more likely to be in poor health and less likely to access needed medical care. Debt-related stress can also negatively influence health behaviors and outcomes.

Acknowledgement: This research was funded by the Annie E. Casey Foundation. We thank them for their support but acknowledge that the findings and conclusions presented in this report are those of the authors alone, and do not necessarily reflect the opinions of the Foundation.

Sycamore takes a neutral and objective approach to analyze and explain public policy issues. Funders do not determine research findings. More information on our code of ethics is available here.

Medical Debt in Tennessee

Medical debt hurt the credit history of an estimated 24% of Tennesseans with a credit report in 2016 (Figure 1), according to a sample of credit bureau data. (1) Nationally, this rate was about 18% with Tennessee having the 10th highest rate among all states.

The median amount of medical debt appearing on Tennesseans’ credit reports was $739. (1) In other words, half of the affected Tennesseans had less than $739 of medical debt on their credit histories, and half had more.

Figure 1

Demographics & Financial Status of Tennesseans with Medical Debt

A 2015 survey suggests unpaid medical bills are common across most demographic and socioeconomic groups in Tennessee, with higher rates likely among certain groups. The 2015 National Financial Capability Study (NFCS) estimated that 27% of Tennesseans age 18-64 had unpaid, past-due medical bills. (3) (4) The survey also estimated that Tennesseans with the following characteristics were more likely to report having past-due medical bills:

- Uninsured*

- Lower income*

- Lower level of education

- Person of color

- No emergency fund*

- Age 35-44

- Children in the household*

About The Data

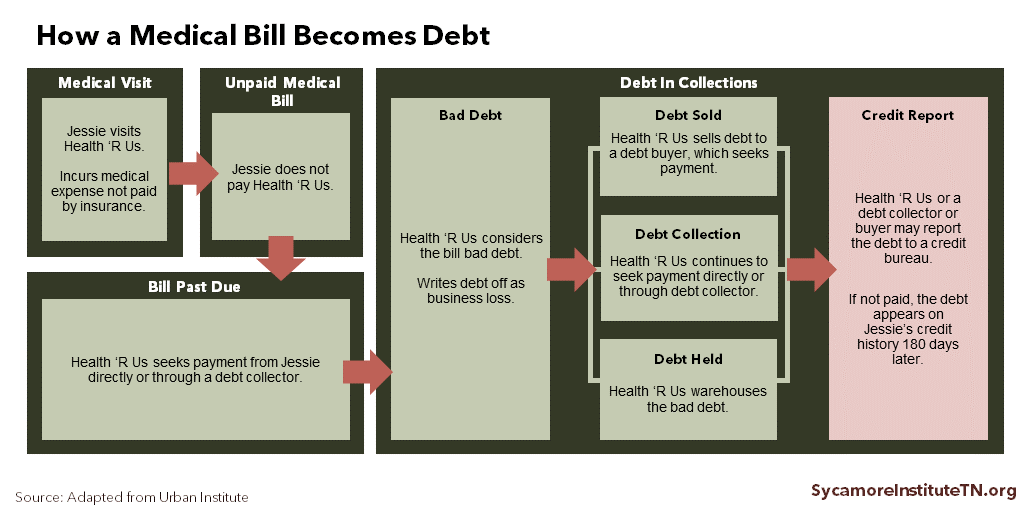

The Credit Bureau Data: The credit bureau data do not include individuals without a credit report or whose unpaid bills have not been reported to a credit bureau (Figure 2). A 2015 study estimated that 11% of adults nationwide do not have a credit report, and those with lower incomes are less likely to have a credit report. (2) As a result, the medical debt estimates based on credit bureau data likely underestimate the prevalence of medical debt in Tennessee.

The NFCS Data: The NFCS estimates are based on survey responses weighted to be representative of each state’s total population, as well as by age, gender, race/ethnicity, and level of education. Due to survey design, results may not be representative of other sub-populations (including those with asterisks above). Medical debt estimates based on the NFCS may over or underestimate the prevalence of medical debt in Tennessee.

See the Methods Appendix for more information about both data sources, their limitations, and the full results of our NFCS analysis.

Figure 2

Medical Debt Affects Prosperity and Health

Medical debt can have long-lasting and compounding effects on economic prosperity and health.

How Medical Debt Affects Financial Security and Economic Mobility

Medical debt can hinder economic security and mobility in both the short- and long-term in a variety of ways. For example, it can:

- Crowd out spending on other basic needs and investments that build long-term wealth.

- Feed a cycle of debt associated with economic stagnation and instability.

- Reduce access to and increase the costs of credit types associated with economic mobility and long-term wealth creation.

- Create barriers to employment and housing.

Medical bills do not have to be huge to create financial challenges. In a national survey by the Federal Reserve, 40% of adults said they would have trouble covering an unexpected $400 expense in 2017. (6) Struggling to pay even small medical bills can pose financial hardship or become the catalyst for other financial problems. (9)

People with medical debt are more likely to have other debts and report trouble paying other bills, meeting basic needs, and saving for the future. Those without resources to pay unexpected medical bills may spend down savings or turn to higher-cost financing methods, which may feed a cycle of debt (see Medical Debt 101). (7) A person with medical debt is more likely to have credit card debt, student loans, car loans, mortgages, and payday loans (i.e. a short-term, high-interest loan). (14) (9) (4) (15) For example, the NFCS estimated that 51% of Tennesseans with unpaid medical bills (vs. 23% without) reported taking a payday loan in the last five years. (3) Medical debt in one’s credit history can also affect financing terms and costs. In addition, some evidence suggests unpaid medical bills may contribute to home foreclosures. (12)

Medical debt hurts credit history and credit scores, which can have wide-ranging and long-lasting effects. Credit history and credit scores affect a person’s access to loans that can enhance economic mobility and long-term wealth (e.g. mortgages). Other potential negative effects include limiting employment opportunities and making access to housing and utility services more expensive. (See Medical Debt 101)

Finally, people with medical debt are more likely to file for bankruptcy. While people file for bankruptcy for multiple reasons, medical debt is often a major contributor in consumer bankruptcies. (16) The extent to which medical debt causes bankruptcy is disputed, but research suggests that low-income households may be more susceptible to bankruptcy resulting from medical debt. (4) (15)

How Medical Debt Affects the Drivers of Health and Health Outcomes

Individuals with medical debt are more likely to be in poor health. (9) (17) (18) Debt in general is associated with higher blood pressure, worse self-reported health status, poorer mental health, and shorter life expectancy. (11) (19) (20) Ultimately, such health outcomes can affect our state’s economy through higher medical costs, lost productivity, and premature death.

These health outcomes may be due, in part, to the wide-ranging effects of debt on the drivers of health. Those drivers include access to clinical care, health behaviors, social and economic factors, and the physical environment.

- People with medical debt are less likely to access needed clinical care or prescription medications than those without medical debt. (10) (21) (22) (17) Individuals may be hesitant to incur additional debt, or providers may refuse service until past-due bills are paid. (8)

- Household debt in general can negatively influence health behaviors. Debt-related stress can lead to risky behaviors like smoking, increased alcohol consumption, and poor nutrition. (23) Aggressive debt collection practices like garnishing wages, property liens, and home foreclosures — which uninsured individuals with lower incomes may be more likely to face — can add to that stress. (24) (25)

- Debt influences our social, economic, and physical environments in ways that can contribute to poorer health outcomes. For example, as discussed in the previous section, medical debt can affect a person’s social and economic status and their housing situation.

Parting Words

Medical debt is a complex topic with far-reaching implications for Tennesseans’ health and prosperity. This report and accompanying Medical Debt 101 primer kick off a series that we hope will inform an evidence-based discussion about medical debt in Tennessee, its effects, and potential policy levers. Subsequent reports will explore county-level data on medical debt in Tennessee and options for policymakers who want to address it.

References

Click to Open/Close

- Ratcliffe, Caroline, et al. Debt in American: An Interactive Map. The Urban Institute. December 6, 2017. Accessed onJanuary 23, 2019 from https://apps.urban.org/features/debt-interactive-map/?type=medical&variable=perc_debt_collect&state=47.

- Brevoort, Kenneth, Grimm, Philipp and Kambara, Michelle. Data Point: Credit Invisibles. Consumer Financial Protection Bureau. May 2015. https://files.consumerfinance.gov/f/201505_cfpb_data-point-credit-invisibles.pdf.

- The Sycamore Institute. Analysis of 2012 and 2015 National Financial Capability Study. FINRA Investor Education Foundation. Data accessed from http://www.usfinancialcapability.org/downloads.php.

- Karpman, Michael and Caswell, Kyle J. Past-Due Medical Debt Among Nonelderly Adults, 2012–15. Urban Institute. [Online] 2017. [Cited: December 12, 2018.] https://www.urban.org/research/publication/past-due-medical-debt-among-nonelderly-adults-2012-15.

- Braga, Breno, et al. Local Conditions and Debt in Collections. Urban Institute. June 2016. https://www.urban.org/sites/default/files/publication/81886/2000841-Local-Conditions-and-Debt-in-Collections.pdf.

- Consumer and Community Development Research Section. Report on the Economic Well-Being of U.S. Households in 2017. Federal Reserve Board, Division of Consumer and Community Affairs. May 2018. https://www.federalreserve.gov/publications/files/2017-report-economic-well-being-us-households-201805.pdf.

- Hamel, Liz, et al. The Burden of Medical Debt: Results from the Kaiser Family Foundation/New York Times Medical Bills Survey. Kaiser Family Foundation. January 2016. https://kaiserfamilyfoundation.files.wordpress.com/2016/01/8806-the-burden-of-medical-debt-results-from-the-kaiser-family-foundation-new-york-times-medical-bills-survey.pdf.

- Seifert, Robert W and Rukanina, Mark. Bankruptcy Is the Tip of a Medical-Debt Iceberg. Health Affairs, 25(2): W89-W92. 2006. https://www.healthaffairs.org/doi/10.1377/hlthaff.25.w89.

- U.S. Consumer Financial Protection Bureau. What is a Payday Loan? June 2, 2017. Accessed on January 28, 2019 from https://www.consumerfinance.gov/ask-cfpb/what-is-a-payday-loan-en-1567/.

- Gross, Tal and Notowidigdo, Matthew J. Health Insurance and the Consumer Bankruptcy Decision: Evidence from Expansions of Medicaid. Journal of Public Economics, 95: 767-778. 2011. http://isiarticles.com/bundles/Article/pre/pdf/48303.pdf.

- Robertson, Christopher Tarver, Egelhof, Richard and Hoke, Michael. Get Sick, Get Out: The Medical Causes for Home Mortgage Foreclosures. Health Matrix: The Journal of Law-Medicine, 18(1).2008. https://scholarlycommons.law.case.edu/healthmatrix/vol18/iss1/4/.

- Austin, Daniel A. Medical Debt as a Cause of Consumer Bankruptcy. Maine Law Review, 67(1): 1-23.2014. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2515321.

- Herman, Patricia M, Rissi, Jill J and Walsh, Michele E. Health Insurance Status, Medical Debt, and Their Impact on Access to Care in Arizona. American Journal of Public Health, 101(8): 1437-1443. 2011. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3134508/.

- Rahimi, Ali R, Spertus, John A and Reid, Kimberly J. Financial Barriers to Health Care and Outcomes After Acute Myocardial Infarction. JAMA, 297(10): 1063-1072. March 14, 2007. https://jamanetwork.com/journals/jama/fullarticle/206020.

- Sweet, Elizabeth, et al. The High Price of Debt: Household Financial Debt and Its Impact on Mental and Physical Health. Social Science and Medicine, 91: 94-100. August 2013. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3718010/.

- Clayton, Maya, Liñares-Zegarra, José and Wilson, John O.S. Can Debt Affect Your Health? Cross Country Evidence on the Debt-Health Nexus. April 2014. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2429025.

- Richardson, Thomas and Roberts, Ron. The Relationship between Personal Unsecured Debt and Mental and Physical Health: A Systematic Review and Meta-Analysis. Clinical Psychology Review, 33(8): 1148-1162. December 2013. https://www.sciencedirect.com/science/article/pii/S0272735813001256.

- Kalousova, Lucie and Burgard, Sarah A. Debt and Foregone Medical Care. Journal of Health and Social Behavior, 54(2): 204-220. 2013. https://journals.sagepub.com/doi/pdf/10.1177/0022146513483772.

- Lessard, Laura and Solomon, Julie. Demographic and Service-Use Profiles of Individuals Using the CarePayment Program for Hospital-Related Medical Debt: Results from a Nationwide Survey of Guarantors. BMC Health Services Research, 16:264. 2016. https://bmchealthservres.biomedcentral.com/articles/10.1186/s12913-016-1525-0.

- Kalousova, Lucie and Burgard, Sarah A. Tough Choices in Tough Times: Debt and Medication Nonadherence. Health Education & Behavior, 41(2): 155-163. 2014.https://journals.sagepub.com/doi/abs/10.1177/1090198113493093.

- Pollitz, Karen and Cox, Cynthia. Medical Debt Among People with Health Insurance. Kaiser Family Foundation. January 7, 2014. https://www.kff.org/private-insurance/report/medical-debt-among-people-with-health-insurance/.

- Drentea, Patricia and Lavrakas, Paul J. Over the Limit: the Association among Health, Race and Debt. Social Science & Medicine, 50: 517-529. 2000.http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.410.5751&rep=rep1&type=pdf.

- O’Teele, Thomas P, Arbelaes, Jose J and Lawrence, Robert S. Medical Debt and Aggressive Debt Restitution Practices: Predatory Billing Among the Urban Poor.Journal of General Internal Medicine, 19(7): 772-778.July 2004. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC1492479/.

- Jacoby, B Melissa and Warren, Elizabeth. Beyond Hospital Misbehavior: An Alternative Account of Medical-Related Financial Distress. Northwestern University Law Review. 2006. https://scholarship.law.unc.edu/cgi/viewcontent.cgi?article=1147&context=faculty_publications.

- Ratcliffe, Caroline, et al. Debt in America: An Interactive Map – Technical Appendix.Urban Institute. December 12, 2018. https://apps.urban.org/features/debt-interactive-map/downloadable-docs/Debt-in-America-Appendix.pdf.

- Applied Research & Consulting LLC. 2015 National Financial Capability Study: State-by-State Survey Methodology. FINRA Investor Education Foundation. July 2016. http://www.usfinancialcapability.org/downloads/NFCS_2015_State_by_State_Meth.pdf.

- Cohen, Robin A and Zammitti, Emily P. Problems Paying Medical Bills Among Persons Under Age 65: Early Release of Estimates From the National Health Interview Survey, 2011–June 2017. National Center for Health Statistics. December 2017. https://www.cdc.gov/nchs/data/nhis/earlyrelease/probs_paying_medical_bills_jan_2011_jun_2017.pdf.

- Batty, Michael, Gibbs, Christa and Ippolito, Benedic. Unlike Medical Spending, Medical Bills In Collections Decrease with Patients’ Age. Health Affairs, 37(8): 1257-1264. 2018. https://www.healthaffairs.org/doi/pdf/10.1377/hlthaff.2018.0349.

Featured image at top by 401(K) 2012