Tennessee’s budget is one of the most significant pieces of public policy our governor and General Assembly tackle each year. Yet understanding what’s in it, why it matters, and how it works can be a challenge.

Sycamore’s Budget Primer explains Tennessee’s finances to help you understand state government and advocate for policies you support. Our signature publication unpacks the process, breaks down the numbers, and explores historical trends using simple language and charts.

Note: Pre-orders are expected to ship near the end of August. Order by August 21 to guarantee a copy.

Download the free PDF version here:

A Preview of What’s Inside

Budget Highlights

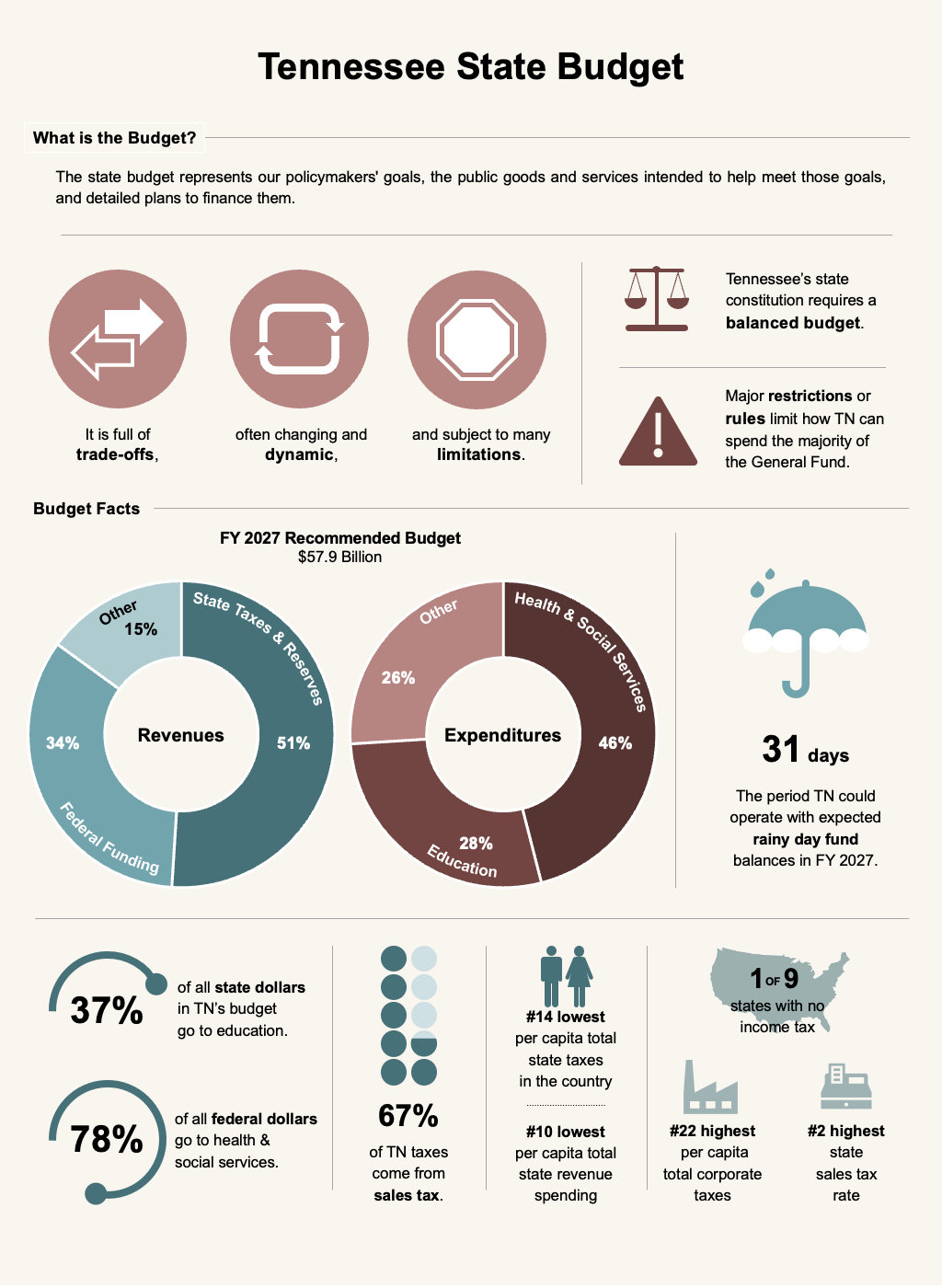

The governor’s FY 2027 recommended budget totaled $57.9 billion. Nearly three-quarters (74%) went toward health and social services (46%) and education (28%). The money primarily came from the state’s own taxes and reserves (51%) and federal funding (34%).

Process

- Fiscal Year – The state’s fiscal year (FY) begins July 1st and ends June 30th.

- Starting Point – Early each calendar year, the governor sends the legislature a recommended budget that builds off the prior year’s recurring base budget. The governor’s recommendation is the starting point for the legislature’s work.

- Balanced Budget Requirement – Tennessee’s constitution requires the budget to balance. This means that spending cannot exceed revenue collections plus reserves each fiscal year.

- Dynamic – To meet this requirement, the budget is often dynamic. As revenue collection estimates change throughout both the planning and spending phases, the budget also changes.

- Budget Management – The executive branch has flexibility to reduce spending and manage the budget to keep it balanced during the fiscal year.

Tennessee’s Annual Budget Cycle

Expenditures

- State Revenue Spending – Funding for programs and activities related to education, general government, capital, public safety, corrections, natural resources, and regulation largely comes from state revenues. Education accounts for 37% of all state dollars in the budget, followed by health and social services at 30%.

- Federal Revenue Spending – Federal dollars fund the lion’s share of health, social services, transportation, and economic development programs and activities. Health and social services account for 78% of all federal dollars in the state budget.

- Overall Spending Levels – Tennessee had the 15th lowest per capita state spending in the U.S. in FY 2025 when accounting for all revenue sources. Its per capita spending from state revenue sources ranked 10th lowest.

- Spending Growth – The extent of growth in Tennessee’s recurring spending depends on how it’s measured. Total and per capita spending reached the highest levels in three decades in FY 2025. As a percent of state personal income and GDP, however, spending fell to historic lows.

Revenues

- Overall Tax Burden – Tennesseans have a relatively low state tax burden. At about $2,970 per Tennessean, the state tax burden was the 14th lowest in the country in FY 2024. Because the state has no income tax, however, many of Tennessee’s other taxes are high compared to those taxes in other states.

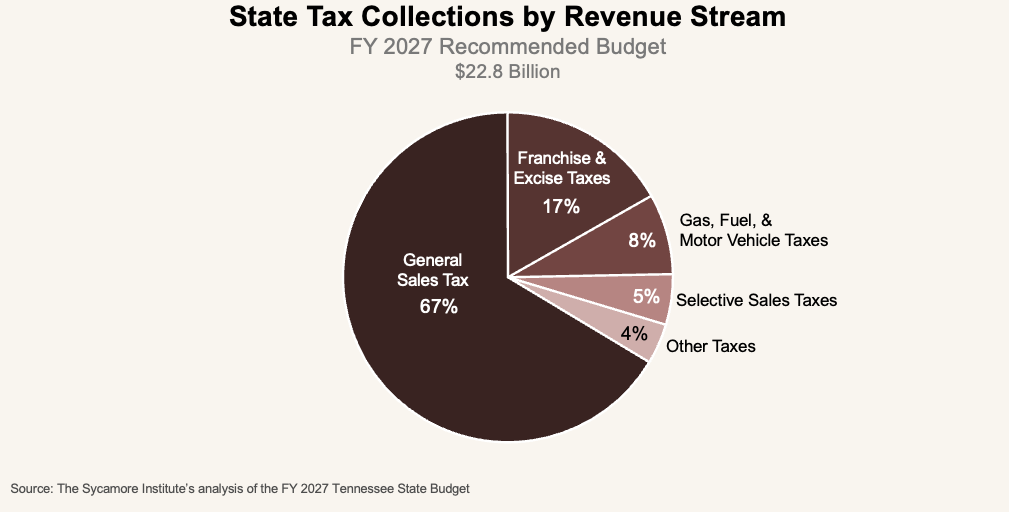

- Sales Tax – The sales tax is Tennessee’s largest source (67%) of state tax revenue. At 7%, Tennessee’s state sales tax rate is the 2nd highest in the U.S.

- Federal Reliance – With 1st being the highest, Tennessee ranks 6th for the share of federal funds in the state budget.

- Strings Attached – Most of the money in the state budget has strings attached—such as programmatic and/or matching requirements for federal dollars, state revenues earmarked for specific purposes, or funding required by lawsuits against the state.

Budget Ups and Downs

- Projecting Revenues – The accuracy of state tax projections plays a major role in whether surpluses and deficits occur. Recent history suggests that making projections is difficult and rarely accurate.

- Surpluses – A surplus occurs when Tennessee has collected more and/or spent less money at the end of a fiscal year than lawmakers budgeted. Not all reserves are surplus, and in fact, most of the state’s unspent reserves are tied up in specific requirements and obligations.

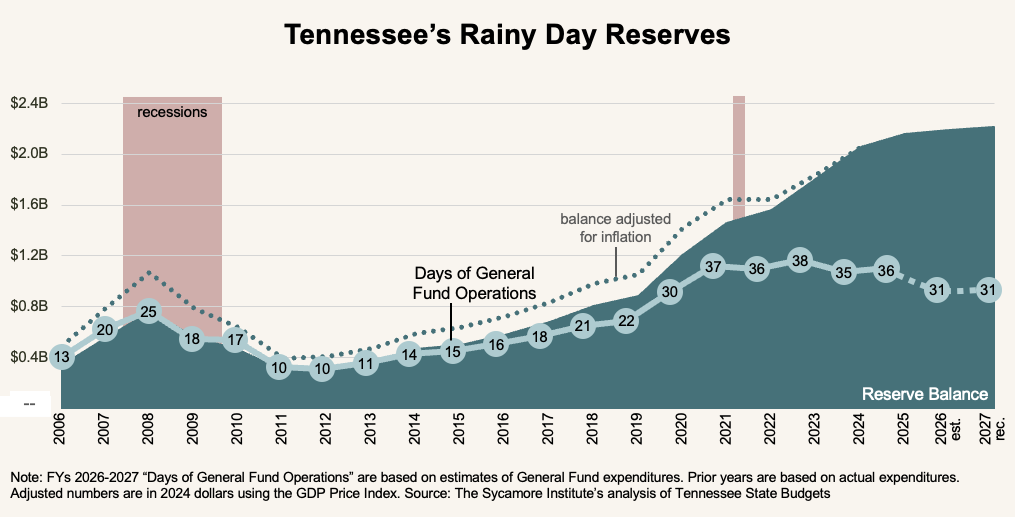

- Recession Readiness – Tennessee could fully fund current state government operations for around 31 days with rainy day reserves alone. That’s about 25% more cushion than the state had going into the Great Recession in FY 2008.

- Rainy Day Best Practices – Tennessee follows most of the best practices when it comes to saving for a rainy day—including defining a purpose in law, setting a target balance, and having rules for replenishment.

- Long-Term Liabilities – Tennessee maintains trust funds to pre-fund long-term liabilities for state employee retiree benefits and is among the top states in the nation for covering these obligations.

Hot Topics

- Structural Issues – Recent budgets highlight structural deficits in a least two areas traditionally funded with dedicated revenues—transportation funding and lottery-funded scholarships.

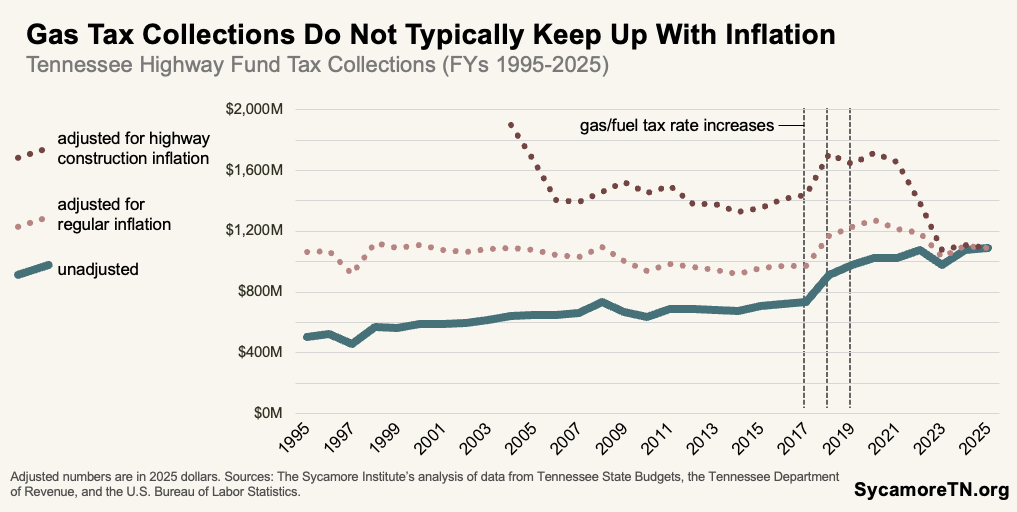

- Inflation – High inflation and its consequences can pose challenges for policymakers managing and balancing the state’s budget. In fact, inflation has grew faster than Tennessee’s state tax collections twice between 2021-2025.

- Federal Matching Requirements – Changes in federal matching requirements can significantly affect the state budget even when the underlying services and enrollment levels remain largely unchanged. Recent examples in TennCare and the Supplemental Nutrition Assistance Program (SNAP) illustrate this dynamic.

- Special Funding Sources – Tennessee policymakers have increasingly relied on dedicated revenue sources and trust funds to support health-related initiatives. This strategy has created opportunities to fund targeted priorities but comes with uncertainty about funding availability and long-term sustainability.