The Tennessee General Assembly is considering proposals to limit how much local policymakers can increase property taxes. Because counties’ property values, tax rates, and reliance on property taxes vary significantly, related statewide policy proposals could affect communities in different ways.

In this post, we share five key insights about local property tax—drawing from Sycamore’s in-depth 2024 analysis Property Tax Capacity and Effort in Tennessee’s 95 Counties. Understanding these details may help policymakers evaluate if and how property tax proposals might influence local budgets, public services, and fiscal flexibility across Tennessee.

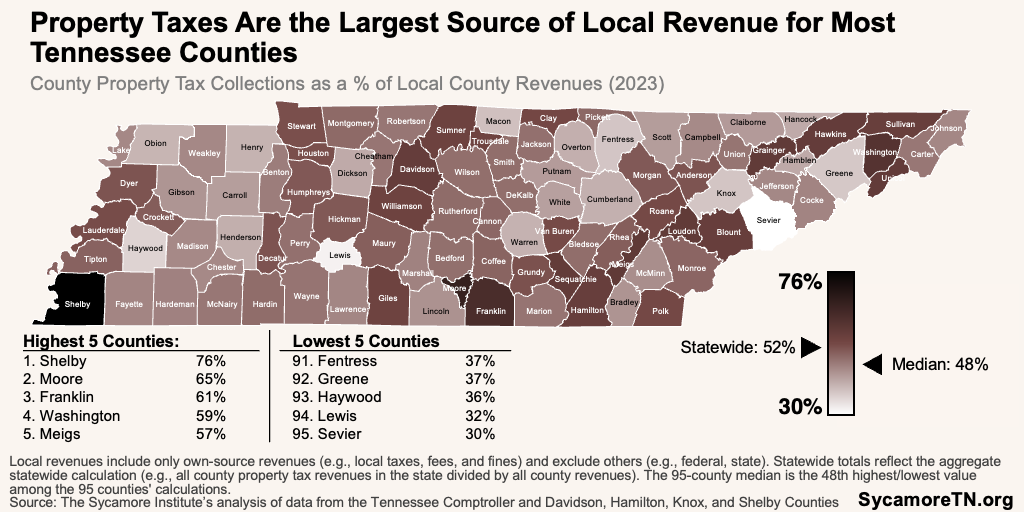

Figure 1

1. Property taxes are the backbone of most county budgets, but reliance varies.

Property taxes are the largest single source of revenue for Tennessee county governments. In FY 2023, counties collected about $5.8 billion in property taxes, which accounted for roughly 52% of total county revenue statewide. (1) (2) (3) (4) (5)

However, counties rely on property taxes to different degrees. In some counties, property taxes make up most local revenues, while others rely more heavily on other sources like local option sales taxes or special taxes and fees. In FY 2023, property taxes varied from 30% of total local revenues in Sevier County to 76% in Shelby (Figure 1). (1) (2) (3) (4) (5)

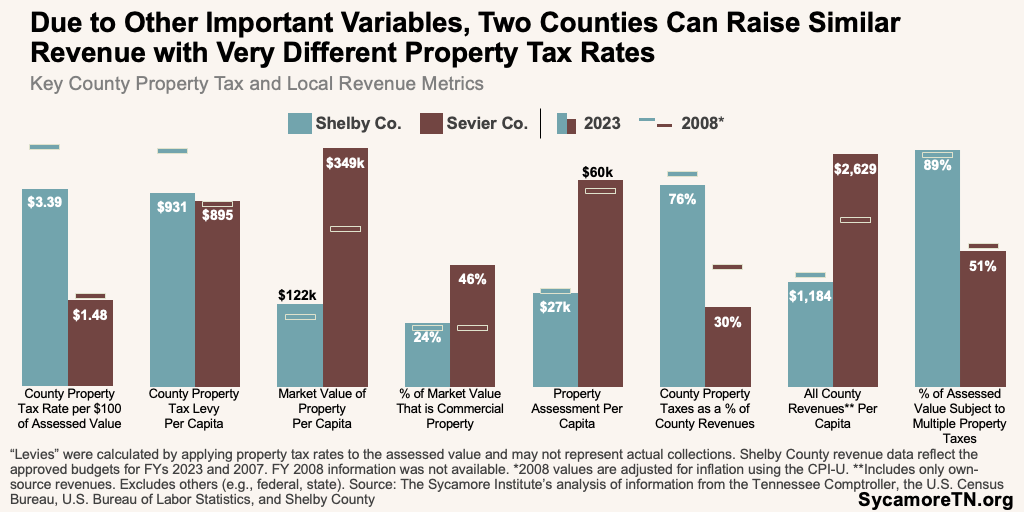

Figure 2

2. Property tax rates alone do not show how much counties actually raise.

Much of the debate around property taxes focuses on rates, but those rates only tell part of the story. For example, two counties can raise similar revenue with very different tax rates due to other variables like property values and the mix of property types.

Tax rates combined with information about the tax base and broader local budget provide a fuller picture of local tax burden. Consider, for example, Shelby and Sevier Counties (Figure 2). In 2023, Shelby’s property tax rate was $3.39 per $100 of assessed value, while Sevier’s was only $1.48. However, Sevier’s lower rate generated only about 4% less[1] per capita than Shelby’s because of significantly higher property value. Sevier had more commercial property value, more of which is subject to tax than other property types. County property taxes also play a larger role in Shelby County government funding than Sevier. Meanwhile, Sevier’s tourism-based economy generates local sales tax revenues, contributing to much higher per capita county revenues than Shelby County. (6) (9) (1) (2)

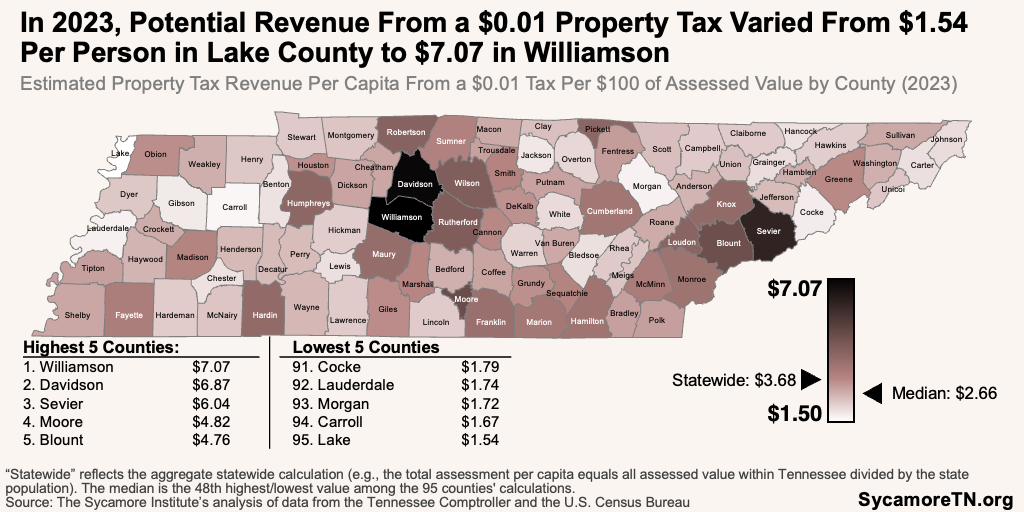

Figure 3

Figure 4

3. Counties’ property tax capacity—and how that has changed over time—varies widely.

The value of taxable property per resident (i.e., property tax capacity) differs dramatically across Tennessee. In 2023, The amount of property value that gets taxed (i.e., the assessed value) varied from a high of $70,676 per capita in Williamson County to a low of $15,365 in Lake. This translates to as much as $7.07 of potential revenue per capita for each $0.01 property tax in Williamson County to $1.54 in Lake County (Figure 3). (6) (9)

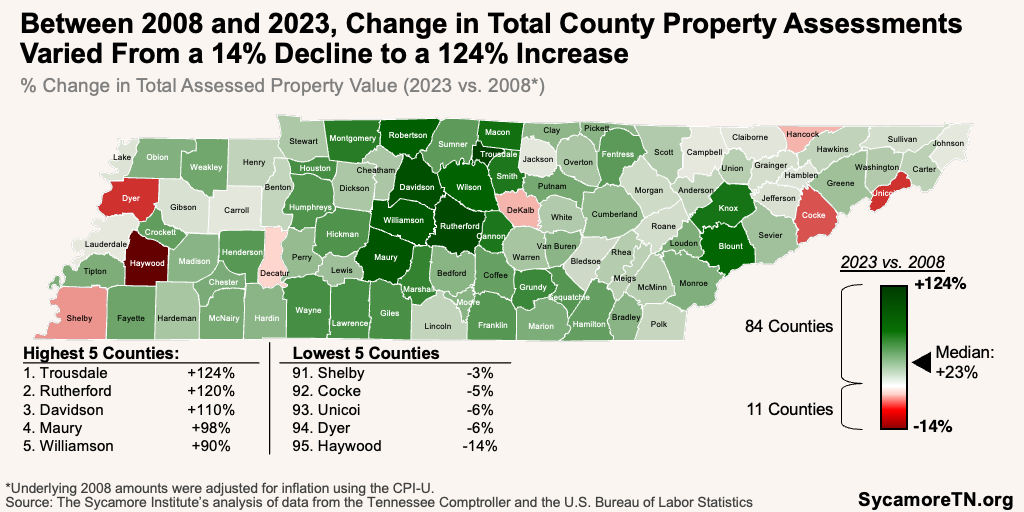

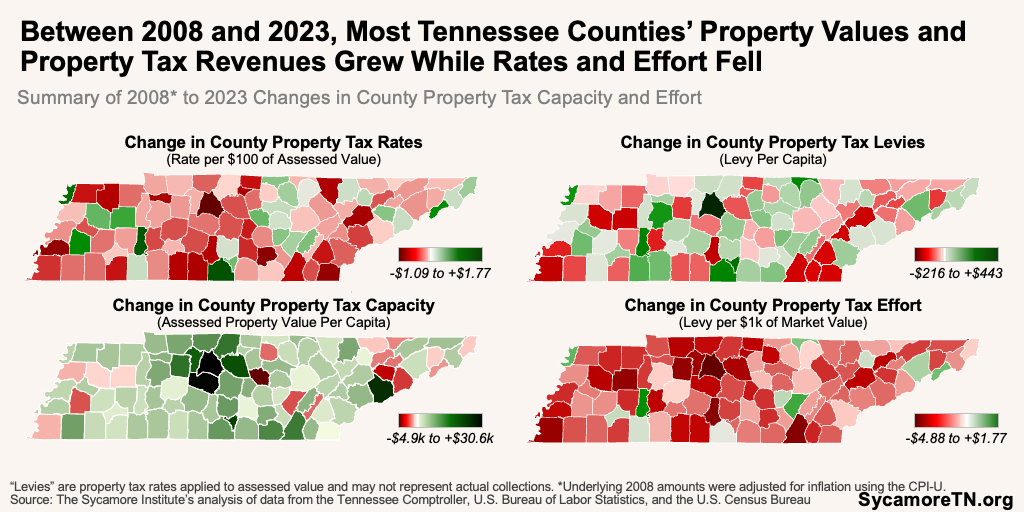

Change in capacity over time also varies widely (Figure 4). For example, counties that experienced strong population growth, development, or commercial investment have generally seen faster increases in property values, while other counties have seen more modest growth. (6) (7) (1) (11) (9) (10) (12) (13)

Figure 5

Figure 6

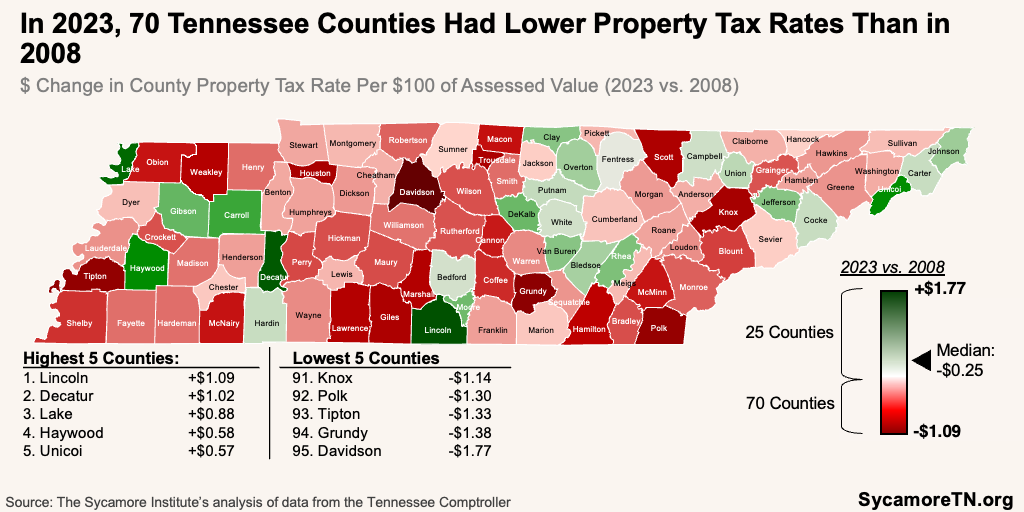

4. Tennessee’s existing certified tax rate requirement shapes property taxes changes and revenues.

Tennessee already places some procedural limits on local property tax increases. State law requires counties to adopt a certified property tax rate after each reappraisal that would generate roughly the same total revenue as the prior year from existing property. (14) (15) Local officials must vote to adopt a higher rate if they want revenues to grow beyond that level. As a result, the majority of counties had lower nominal tax rates in 2023 than they did in 2008 (Figure 5). (9) (7) (11) (10)

The effect and degree of recent property tax rate changes were not uniform across the state (Figure 6). For example, tax rates tended to fall more in counties where property values increased the most—even as they maintained or grew their property tax revenues. (9) (7) (10) (11)

5. Proposed limits on property tax rate increases could affect communities differently.

Because counties differ significantly in their property tax bases, growth patterns, and other revenue sources, policies limiting rate increases could have different effects across communities. For example, some counties may see new revenue from rapid growth in property values or new development while others with slower property value growth may rely more on periodic rate adjustments to maintain revenues over time. Understanding these differences can help policymakers evaluate how proposals to limit property tax rate increases could affect their local communities.

[1] Measured as property tax levy, which equals the total amount of assessed property value within a taxing authority’s jurisdiction multiplied by that authority’s property tax rate. Levies/levy revenues per capita allow for comparisons across counties. These terms do not refer to actual collections and do not reflect actual or average tax bills or burden.

References

Click to Open/Close

References

- Tennessee Comptroller of the Treasury. Transparency and Accountability for Governments (TAG) Exports – Revenues 2007-2023. Local Government Audit. [Online] https://comptroller.tn.gov/office-functions/la/e-services/tag-tableau/tag-exports.html.

- Shelby County Tennessee. Adopted Budget Fiscal Year 2023 Countywide All Funds Summary. [Online] https://www.shelbycountytn.gov/Archive.aspx?ADID=12212.

- The Metropolitan Government of Nashville and Davidson County. Annual Comprehensive Financial Report For The Year Ended June 30, 2023. [Online] June 2024. https://www.nashville.gov/sites/default/files/2024-06/2023_Annual_Comprehensive_Financial_Report_Final_6.25.24.pdf?ct=1719506888.

- Hamilton County Tennessee. Annual Comprehensive Financial Report For The Year Ended June 30, 2023. [Online] March 2024. https://comptroller.tn.gov/content/dam/cot/la/advanced-search/2023/other/1478-2023-CN-hamiltonco-rpt-cpa764-3-25-24.pdf.

- Knox County Tennessee. Annual Comprehensive Financial Report For The Year Ended June 30, 2023. [Online] June 2024. https://comptroller.tn.gov/content/dam/cot/la/advanced-search/2023/other/1492-2023-cn-knoxco-rpt-cpa225-1-31-24.pdf.

- Tennessee Comptroller of the Treasury. 2023 Tax Aggregate Report of Tennessee. State Board of Equalization. [Online] https://comptroller.tn.gov/content/dam/cot/pa/documents/tax-aggregate-reports/2023TaxAggregateReport.pdf.

- —. 2008 Tax Aggregate Report of Tennessee. State Board of Equalization. [Online] Provided to The Sycamore Institute upon request.

- Shelby County Tennessee. Adopted Fiscal Year 2007 Countywide Summary. [Online] https://www.shelbycountytn.gov/Archive.aspx?AMID=&Type=&ADID=78.

- U.S. Census Bureau. Annual Estimates of the Resident Population for Counties: April 1, 2020 to July 1, 2023 (CO-EST2023-POP). [Online] 2023. https://www.census.gov/data/tables/time-series/demo/popest/2020s-counties-total.html.

- —. Intercensal Estimates of the Resident Population for Counties: April 1, 2000 to July 1, 2010. [Online] 2010. https://www.census.gov/data/tables/time-series/demo/popest/intercensal-2000-2010-counties.html.

- U.S. Bureau of Labor Statistics. U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All Items in U.S. City Average [CPIAUCSL]. Retrieved from FRED, Federal Reserve Bank of St. Louis. [Online] https://fred.stlouisfed.org/series/CPIAUCSL.

- U.S. Census Bureau. 2022 Small Area Income and Poverty Estimates (SAIPE). [Online] https://www.census.gov/data-tools/demo/saipe/#/?s_state=47&s_county=&s_district=&s_geography=county&s_measures=mhi.

- —. County-Level Urban and Rural information for the 2020 Census. [Online] September 2023. https://www.census.gov/programs-surveys/geography/guidance/geo-areas/urban-rural.html.

- Tennessee Comptroller. Property Tax Reappraisal and Certified Tax Rate. State Board of Equalization. [Online] https://comptroller.tn.gov/boards/state-board-of-equalization/sboe-resources/certified-tax-rate.html.

- Green, Harry, Chervin, Stan and Lippard, Cliff. The Local Government Finance Series, Volume I: The Local Property Tax in Tennessee . Tennessee Advisory Commission on Intergovernmental Relations (TACIR). [Online] February 2002. https://www.tn.gov/content/dam/tn/tacir/documents/LOCAL_PROPERTY_TAX.pdf.